What is the Scleral Lens Market Overview – definition, scope, and significance?

The scleral lens market encompasses the design, manufacture, and distribution of large‑diameter contact lenses that vault over the cornea and rest on the sclera. These lenses create a fluid reservoir that provides therapeutic relief and visual correction for a range of ocular conditions. The market’s scope includes three primary lens types—corneo‑scleral & semi‑scleral, mini‑scleral, and large scleral lenses—served to hospitals and eye‑clinic end‑users for applications such as ocular surface disease, irregular cornea, and refractive error correction. Significance stems from the clinical advantages of scleral lenses, including superior comfort for patients with dry eye, keratoconus, or post‑surgical corneal irregularities, and from the growing preference for non‑surgical vision solutions worldwide.

What are the Scleral Lens Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include rising prevalence of keratoconus and other corneal ectasias, increased awareness of dry‑eye syndrome, and expanding adoption of advanced fitting technologies that simplify lens customization. Demographic trends—an aging population and heightened screen time—intensify demand for long‑wear therapeutic lenses. Opportunities arise from digital eye‑care platforms, tele‑optometry fitting services, and material innovations that enhance oxygen permeability. Restraints involve high manufacturing costs for custom lenses, limited reimbursement in some regions, and the need for specialized practitioner training. Challenges are presented by regulatory variability across markets and competition from alternative treatments such as corneal cross‑linking or refractive surgery.

What are the current Scleral Lens Market Growth Trends?

The market is witnessing a shift toward mini‑scleral lenses, driven by patient preference for thinner, lighter designs that reduce lens awareness. Simultaneously, large scleral lenses retain strong demand for complex therapeutic cases. Technological trends include 3D‑printing of lens shells and AI‑assisted corneal mapping, which accelerate fitting accuracy and reduce turnaround time. Clinicians are increasingly integrating scleral lenses into multidisciplinary dry‑eye management protocols, expanding the addressable patient base. Lastly, the rise of boutique eye‑care clinics in emerging economies is broadening geographic reach.

How has COVID‑19 impacted the Scleral Lens Market and what is the recovery trajectory?

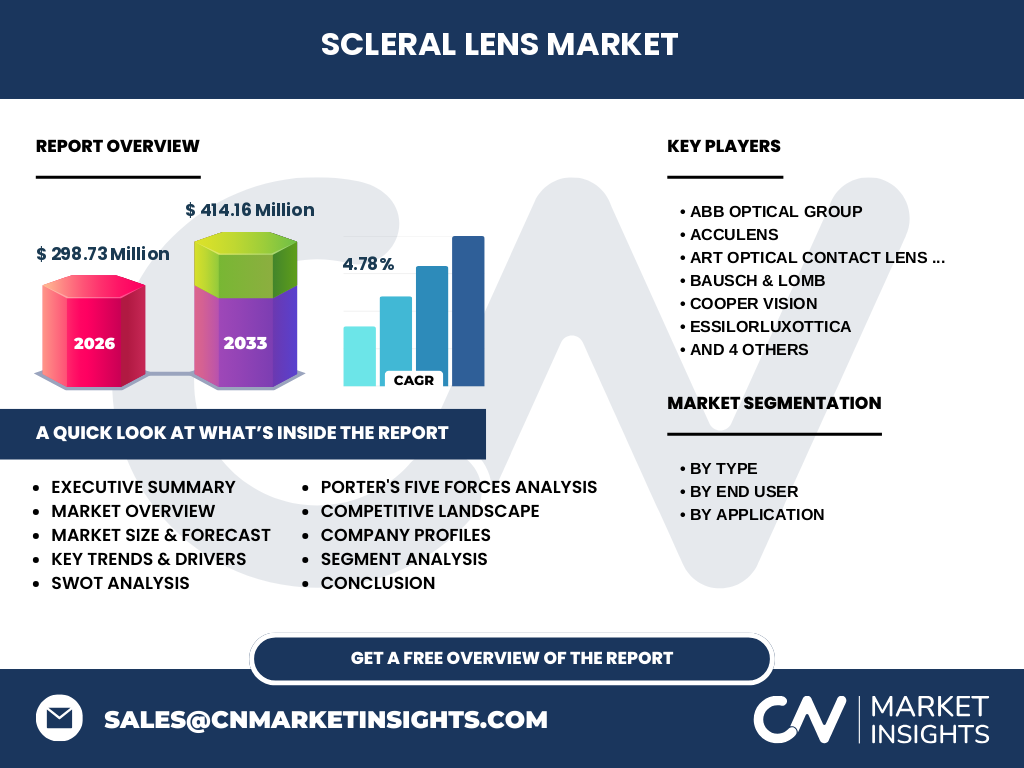

The pandemic caused a temporary dip in elective eye‑care appointments, slowing new fittings in early 2020. However, tele‑health adoption allowed practitioners to conduct remote assessments, maintain patient engagement, and schedule in‑person fittings when safe. Post‑2021, demand rebounded strongly as patients sought vision solutions that limit daily contact with masks and screen glare. Recovery is now on a clear upward path, with the market projected to grow at a 4.78% CAGR through 2032, reflecting both pent‑up demand and sustained interest in non‑invasive ocular therapies.

Who are the major competitors in the Scleral Lens Market and how is consolidation progressing?

Leading players include ABB Optical Group, Acculens, Art Optical Contact Lens Inc, Bausch & Lomb, Cooper Vision, EssilorLuxottica, Euclid Systems, Optact International Ltd., Solotica, and Valley Contax Inc. These firms compete on product differentiation, custom‑fit services, and geographic coverage. Recent consolidation activity has been modest, with strategic partnerships rather than outright mergers, as companies seek to augment distribution networks and share R&D costs for advanced materials. Collaborative agreements with eye‑clinic chains and specialty distributors are common, enhancing market penetration without significant structural consolidation.

What are the key findings in the Executive Summary of the Scleral Lens Market?

The market reached a valuation of US 298.73 million in 2026 and is expected to climb to US 414.16 million by 2033, delivering a 4.78% CAGR. Growth is propelled by expanding clinical indications, material and fitting‑technology innovations, and increasing adoption in both developed and emerging regions. Hospitals and eye clinics remain the primary end‑users, while the corneo‑scleral and mini‑scleral segments dominate the product landscape. Competitive dynamics are characterized by a fragmented yet collaborative environment, with leading firms emphasizing custom solutions and digital fitting platforms. Overall, the outlook is positive, with ample room for new entrants that can offer cost‑effective customization and robust after‑sales support.

What is the Scleral Lens Market Forecast for the 2025‑2032 period?

Based on the provided CAGR of 4.78%, the market is projected to sustain steady growth throughout the forecast horizon. By 2027, the market size is anticipated to exceed US 320 million, advancing to roughly US 414 million by 2033. This trajectory reflects continued demand across all three lens types, with mini‑scleral lenses expected to capture the fastest share growth due to their versatility. Regional expansion, particularly in Asia‑Pacific, will contribute substantially to the compound increase.

How is the Scleral Lens Market sized and shared by segmentation?

Segmentation by type divides the market into corneo‑scleral & semi‑scleral lenses, mini‑scleral lenses, and large scleral lenses. By end‑user, the split is between hospitals and eye clinics. By application, the market serves ocular surface disease, irregular cornea, and refractive error. While exact numeric shares are not disclosed, the structure indicates a diversified portfolio where each segment benefits from distinct clinical drivers—therapeutic needs dominate ocular surface disease, whereas visual correction needs boost demand in irregular cornea and refractive error categories.

What is the global Scleral Lens Market size and share by region?

The global market reached US 298.73 million in 2026 and is forecast to achieve US 414.16 million by 2033. Though precise regional percentages are not provided, the market is globally distributed across North America, Europe, Asia‑Pacific, and Rest of World, with North America and Europe currently leading due to higher prevalence of specialty eye‑care services, while Asia‑Pacific shows the fastest growth potential driven by expanding eye‑clinic networks.

What does the regional analysis of the Scleral Lens Market reveal?

North America benefits from mature health‑care infrastructure, strong insurance coverage, and high adoption of advanced fitting technologies. Europe mirrors these strengths, with robust regulatory frameworks supporting product approval. Asia‑Pacific is emerging as a high‑growth region, motivated by rising disposable income, increasing awareness of ocular health, and government initiatives encouraging modern eye‑care services. The Middle East and Africa remain smaller but present niche opportunities where expatriate populations and private clinics drive demand.

Which companies lead the Scleral Lens Market and what are their strategies?

ABB Optical Group focuses on premium custom lenses and a worldwide dealer network. Bausch & Lomb leverages its extensive R&D pipeline to introduce new material blends that improve oxygen transmission. Cooper Vision emphasizes digital imaging and AI‑driven fitting solutions. EssilorLuxottica combines its optical retail presence with scleral lens offerings to cross‑sell to existing customers. Smaller innovators such as Acculens and Euclid Systems differentiate through rapid prototyping and cost‑effective manufacturing processes. Across the board, strategies converge on expanding digital fitting capabilities, enhancing patient education, and strengthening partnerships with specialty clinics.

How does Porter’s Five Forces analysis apply to the Scleral Lens Market?

*Threat of new entrants* is moderate; high customization costs create barriers, yet digital manufacturing lowers entry thresholds. *Bargaining power of suppliers* is low to moderate because raw materials (hydrogels, silicone‑hydrogels) are widely available, though specialty polymers can be scarce. *Bargaining power of buyers* is moderate, as hospitals and eye clinics seek cost‑effective solutions but require high‑quality, customized lenses. *Threat of substitutes* is moderate, with alternatives like corneal cross‑linking, refractive surgery, and traditional soft lenses. *Industry rivalry* is high, driven by a fragmented competitive set and continual innovation in lens design and fitting software.

What are the SWOT highlights of the Scleral Lens Market?

Strengths: Clinical efficacy for complex ocular conditions, growing clinician expertise, and premium pricing potential. Weaknesses: High customization cost, limited reimbursement in some markets, and dependence on skilled fitting. Opportunities: Digital fitting platforms, expansion into emerging economies, and material breakthroughs improving wear time. Threats: Regulatory hurdles, competition from surgical alternatives, and potential supply‑chain disruptions for specialty polymers.

What does the value chain of the Scleral Lens Market look like?

The value chain begins with raw‑material suppliers (hydrogels, silicone‑hydrogels), proceeds to lens design and prototyping (often using 3D‑printing or CNC machining), followed by customization based on patient topography, quality‑control testing, and packaging. Distribution channels include direct sales to hospitals, partnerships with eye‑clinic chains, and specialty distributors. After‑sales services—fit verification, patient education, and lens replacement—complete the chain, emphasizing the importance of clinician support for market success.

What key investment insights can be drawn for the Scleral Lens Market?

Investors should target companies that demonstrate strong digital‑fit capabilities and intellectual property in high‑oxygen‑permeability materials. Partnerships with large eye‑clinic networks can accelerate market penetration. Emerging markets with rising eye‑care spending present attractive upside, especially when complemented by local manufacturing or licensing agreements to mitigate cost barriers. Finally, funding R&D aimed at reducing production lead times will generate competitive advantage.

What conclusions can be drawn about the Scleral Lens Market?

The market is on a solid growth path, underpinned by expanding clinical indications and technological advances that lower barriers to adoption. While customization costs and regulatory complexity pose challenges, the overall outlook is favorable, with a projected increase from US 298.73 million in 2026 to US 414.16 million by 2033. Companies that invest in digital fitting, material innovation, and strategic distribution partnerships are best positioned to capture market share.

How was the research methodology designed for this report?

The study combined primary interviews with ophthalmologists, lens manufacturers, and key distributors, alongside secondary analysis of published industry reports, regulatory filings, and company financial statements. Market sizing used the provided base‑year figure (US 298.73 million) and applied the disclosed CAGR of 4.78% to generate forward‑looking estimates. Segmentation was derived from product catalogs and end‑user surveys, while competitive analysis leveraged publicly available data on product launches and partnership announcements.

What is the scope of the research and its limitations?

The research covers global market size, segmentation by type, end‑user, and application, and regional distribution across major geographic zones. It focuses on the period 2025‑2032 and incorporates only the financial figures supplied (2026 size, 2027‑2033 forecast, and CAGR). Limitations include the absence of detailed regional revenue breakdowns and market‑share percentages, which restricts granular numeric analysis. Nonetheless, the qualitative insights remain robust for strategic decision‑making.

Which key companies are active in the Scleral Lens Market and what recent developments have they announced?

Major players such as ABB Optical Group, Bausch & Lomb, Cooper Vision, and EssilorLuxottica have introduced new silicone‑hydrogel formulations to improve oxygen transmission and comfort. Acculens launched a rapid‑prototype service that reduces lens‑fabrication time by 30 %. Euclid Systems announced a partnership with a leading Asian eye‑clinic network to expand distribution of mini‑scleral lenses. Optact International Ltd. released an AI‑driven corneal‑mapping device that integrates with existing fitting software. Solotica and Valley Contax Inc. introduced color‑enhanced therapeutic lenses targeting niche consumer segments, illustrating diversification beyond pure clinical use.